Abstract

Regional Cooperation in South Asia has been a slow-moving process due to numerous reasons, the most prominent of which is the India- Pakistan conflict. This has led scholars to explore new ways of cooperation. One such concept is the concept of sub-regional cooperation excluding either of the two conflicting countries. This paper reviews the existing energy sector of the BBIN countries on an individual basis and then intends to explore the prospects and benefits of sub-regional cooperation in the energy sector in a multilateral arrangement among the four countries - Bangladesh, Bhutan, India and Nepal.

Energy is one of the basic needs for development of any country. The energy demand in the South Asian region is expected to grow at an annual rate of 5%. (Rahman et al., 2012) The SAARC has come to a deadlock because of the Indo-Pak conflict. Eastern South Asia is a sub-region which has gained attention in recent times for enhancing cooperation among countries in South Asia. The sub-region includes Bangladesh, Bhutan, India and Nepal. Some literature also includes Myanmar or Tibetan part of China. In this paper, only those countries in the eastern part of South Asia which are part of SAARC will be considered as eastern South Asia.

Being developing nations, these countries face a growing demand for energy. All the four countries are heavily dependent on energy. Energy holds a prominent position in their EXIM trade basket. Constant increase in imported energy sources such as coal, gas and oil have an adverse impact on the energy security of the sub-region. This sub-region is equipped in producing almost all kinds of energy (hydro, thermal, wind, solar). Some of these energy generation is affected seasonally. But the countries in the sub-region have the geographical advantage of having contiguous borders with each other. The willingness of subregional political regime is the most significant factor for enhancing sub-regional cooperation in supply of fossil fuel and energy trading.

A general analysis of the needs and potential of individual country would give a clear picture for assessing whether a cooperation as the sub-regional level is feasible and beneficial. The sub-region taken into consideration in this paper includes India (especially eastern part of India), Bangladesh, Nepal and Bhutan. The study would delve into the potential that the Eastern South Asia hold for energy cooperation in order to strengthen energy security in the sub-region. Strengthening ties among the countries of Eastern South Asia creates new hope of greater integration in the region.

Energy Overview of India

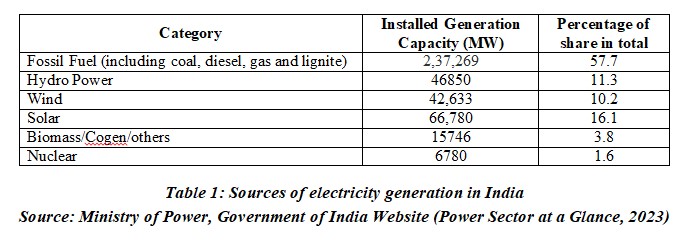

India has a diversified energy mix to generate power. These include biomass, solar, wind, small hydro, hydro, natural gas, and nuclear power. As on February 2023, the generation capacity of India is 412 GW.(CEA, 2023). India is heavily dependent on coal for its energy needs. India has become a power surplus nation with no scarcity of coal or electricity, the power minister said in June 2017.(PIB, 2017) Thermal energy is a significant part of India’s energy mix. Out of the total energy capacity, the energy generated from fossil fuels including coal is 57.7 percent. (Power Sector at a Glance, 2023)

In April 2018, Indian government announced 100% electrification of its rural areas has been completed. (The Wire, 2018) But electrification of all households is yet to be achieved. Moreover, electrification does not mean that there is 24-hours power supply in those areas. The duration of supply of electricity for domestic use in about 53% of the villages is less than 12 hours per day.(Mishra, 2019) There has been an improvement in rural electrification, but the quality of energy supply is still very poor.

In order to meet the growing demand, India imports coal. Coal is the fourth largest commodity imported by India. The total value of coal imported in 2021 amounts to 25710.2 million US$. (UNCOMTRADE, 2022) The value of petroleum gas and other hydrocarbon gases imported in the year 2021 amounts to 24044.6million US$. India imports crude petroleum too and refines it in the refinaries. The refineries have the capacity to process more than the demand in India. The surplus refined petroleum products are exported to Bhutan Nepal, Bangladesh and other countries. India’s import of crude petroleum oil amounts to US$106406.8million. Refined petroleum is the export product of the highest value in the export basket of India. It amounts to US$54037.1million. (UNCOMTRADE, 2022)

Majority of the energy requirement is covered by thermal power stations (TPS). But some of the thermal power plants are becoming NPA (non-performing assets) and one of the reasons is the shortage in the supply of coal.(Mishra, 2019) Poor financial state of the discoms has led to shortage in fuel supply, poor quality of supply to the consumers and inability of power producers to efficiently sell power in the market leading to heavy losses for the producers. To deal with such problems, in 2019, India’s Central Electricity Authority (CEA) has collaborated with Japan Coal Energy Center (JCOAL) to study about improving the efficiency and environmental improvement of coal fuelled power plants. India is also gradually moving to alternative sources of renewable energy in order to reduce the imports of energy fuels and to improve the Balance of Payments.

With regard to renewable energy, India has great potential to generate wind energy because of its 7600 km long coastline. The states of Gujarat and Tamil Nadu have the highest potential to develop wind energy. and solar energy and other sources of renewable energy. Wind energy has about 10 percent share in the overall generation capacity of India. Solar energy too is abundantly available in India. About 5,000 trillion kWh per year solar energy is incident over India's land area. Theoretically, a small fraction of the total incident solar energy (if captured effectively) can meet the entire country's power requirements. But solar energy has a share of about 16 percent in the total generation capacity of India. As on 31st March, 2021, Karnataka and Rajasthan have the highest installed capacity for solar power generation.

Nevertheless, there is marginal deficit of 0.4 percent in energy supply in 2021-22. The peak deficit of energy was 1.2 percent. India therefore needs to ensure energy security by cooperating and collaborating with private sector and neighbouring states with high potential and also by harnessing its untapped renewable energy resources.

Energy Overview of Bangladesh

Natural gas and coal are the primary energy sources used to generate electricity in Bangladesh (Al-tabatabaie et al., 2022). In Bangladesh, electricity is available for 85 percent of the population.(International Energy Agency, 2023) In Bangladesh, oil, gas and coal are the main fuels for electricity generation. Apart from that, natural gas is also used for fertiliser industry. Natural Gas has a majority share in the energy mix of Bangladesh. About 58% of the domestic power demand is met by natural gas. (Bangladesh Power Development Board, 2019) The gas reserves in Bangladesh are depleting. In order to meet the growing demand, the country is importing gas from Qatar. At the same time, new renewable sources like solar, wind energy and hydro energy for electricity generation are being explored. Bangladesh imports coal from India.

The total electricity demand in 2021 was around 20 GW (Ministry of power energy and mineral resources). To meet the increasing demand and to address the depleting resources, Bangladesh has number of projects in its pipeline. In Bangladesh, renewable energy has advanced significantly in recent years. A feasibility study to analyse its wind energy potential was conducted in collaboration with the Netherlands. .(Faijer & Arends, 2017) By 2030, the Bangladeshi government plans to produce more than 4100 MW of power from renewable sources. (Al-tabatabaie et al., 2022) With the commissioning of 360 MW Haripur and 450 MW Meghna Ghat and Power plants built by the private sector with foreign investment, Bangladesh achieved 100% electrification.(Dhaka Tribune, 2022)

It is constructing its first nuclear power facility in Roopur with technical and financial support from Russia. (Gyanwali et al., 2021) It has an expected generation capacity of 2.4 GW by 2024. An LPG pipeline is being negotiated among India, Bangladesh and Myanmar (IBM). Hydro power in Bangladesh has very little scope because of its concern for land use and flooding. However, Bangladesh is planning to import hydro power from Nepal through India.

Energy Overview of Nepal

Being situated in the Himalayas, Nepal has abundant potential for hydropower. Hydropower is the main source of electricity in the country. About 94% of the population have access to electricity. Nepal has not yet fully harnessed its hydropower potential. It is capable of producing more energy than required within the country. Therefore, energy trading is a possibility for Nepal to earn forex by exporting energy to India and Bangladesh. Currently, Nepal is dependent on India for fossil fuels like petrol and diesel as it does not have fossil fuel reserves or production capacity.

Most of the hydropower plants in Nepal are run-of-river (ROR) projects. This makes Nepal vulnerable to irregular and erratic supply of electricity based on seasonal climatic changes. The electricity generation is less than 40% during winter. Nepal has four major rivers: the Saptakoshi, Narayani, Karnali and Mahakali, and their tributaries originate either from the Himalayas or from the Tibetan Plateau.(Jha, 2010) Nepal has a shortage of technical human resources and financial resources. Hence it is unable to harness its hydro power generation capacity to its full potential. Nepal currently producing 2,000MW of electricity, of which 1,900MW is generated from hydropower projects.

Private sector enterprises and even foreign investments are being utilised for constructing hydro storage projects and power trade agreements are being established with neighbouring countries. For example, a trilateral cooperation mechanism consisting of Nepal, India and Bangladesh (NIB) has been agreed upon. The Upper Karnali hydropower project is a run-of-the-river hydropower project being developed on Karnali River in Nepal. The project will supply power to Nepal, India, and Bangladesh for a contracted period of 25 years. The Government of Nepal awarded the project to GMR Upper Karnali Hydro Power Limited (GUKHL), a subsidiary of GMR Group India in 2008. GMR is developing the project on a build-own-operate-transfer (BOOT) basis. (The Himalayan Times., 2019). According to the agreement, Nepal will get 12% free power from the total power generated by the project, while Bangladesh will buy 56 percent and India will buy the remaining 32%. This project is looked upon as a steppingstone towards enhancing cooperation in the energy sector which may have a dominos effect for similar collaboration in other sectors as well.

Energy Overview of Bhutan

The power system of Bhutan is dominated by indigenously produced hydropower with an installed capacity of 1.6 GW. The majority of potential sites are concentrated in the Wangchhu, Punatsangchhu, Mangdechhu and Drangmechhu river basins.(Gyanwali et al., 2021) All these rivers are perennial in nature. Its flow is determined by melting of snow from the high Himalayan ranges. Therefore, they have the potential for developing hydro-power projects. Bhutan is self-sufficient in meeting its electricity needs. It has achieved 100 percent electrification of its households. It has utilised only 2 percent of its hydropower capacity. It imports refined petroleum products, gas and coal from India. The Bhutanese people depend on firewood for primary energy and it contributes to 90% of energy consumption.

The Bhutanese government has adopted clean energy policy to develop its carbon-neutral hydropower in order to meet its domestic demand and to export the surplus power to neighbouring countries. Bhutan and India signed the Agreement on Cooperation in the Field of Hydroelectric Power (HEP) in July 2006. Bhutan exports hydropower energy to the Indian state, West Bengal. In collaboration with India, Bhutan is developing numerous hydropower projects. One such project is run-of-the-river 1,020 MW Punatsangchhu-II Hydroelectric Project (PHEP-II). The project is expected to become operational by October 2024. It will generate 4357 million units of electricity annually increasing Bhutan’s power generation capacity by 43 percent.(Kuensel, 2022)

Prospects for Sub-Regional Energy Cooperation

Mutual co-existence and intra-regional energy trading is the key to ensuring energy security in the sub-region. Access to steady supply of electricity is the fundamental aspect of energy security.

The average per capita energy use of BBIN is about 0.6 tonnes of oil equivalent (TOE) which is far below the global average (Gyanwali et al., 2021). Petroleum products and gas in this sub-region is very limited. This compels the sub-regional countries to rely heavily on imported fossil fuels.

Nepal and Bhutan have abundant potential to meet their energy needs as well as engage in energy trading through hydropower projects. But Nepal has been able to accomplish only 89 percent of electrification (World Bank, 2023). Bhutan has become fully capable of meeting its energy demands since 2016. Bhutan has used only 2% of its hydropower generating capacity. It has met all the energy needs of its population. Whereas Bangladesh which is downstream has energy shortage. Only 70% of its energy needs have been met. Thus, the potential to supply for the shortfall of energy exists within the sub-region. India and Bangladesh are heavily dependent on coal based and other non-renewable energy resources. India is energy deficit during peak season and is mainly dependent on thermal energy which is not environment friendly. This deficit can be met by the excess supply of clean hydro energy from Bhutan and Nepal. Bhutan and Nepal are 100% dependent on India for coal, oil and gas.

Among renewable sources, solar energy generation too has great potential in all these four countries because of their proximity to the Tropic of Cancer. Lack of financial, technical and infrastructural facilities are the basic reasons for underutilisation of resources. These hurdles can be overcome by energy trading among the four countries in the sub-region.

Current Scenario in Sub-Regional Energy Cooperation

Energy trading has two components. Firstly, there is trading of indigenously extracted coal and refined petroleum products from India to Nepal, Bhutan and Bangladesh. This petroleum is imported in crude form from other regions of the world and refined in Indian refineries. Secondly there is trading of indigenous hydropower from Nepal and Bhutan to India and Bangladesh.

The recent developments in the hydrocarbon energy trading are encouraging. Nepal in collaboration with India constructed South Asia’s first petroleum pipeline between India and Nepal. It started functioning in September, 2019. It carries petroleum products from Motihari in Bihar (India) to Amlekhgunj in Nepal. It is 69 km long and has a capacity to transport 2 million metric ton per annum (MMTPA). (PIB, 2019)

In March, 2023, a new pipeline called India – Bangladesh Friendship Pipeline (IBFP) was inaugurated between India and Bangladesh for transportation of diesel from India to Bangladesh. It has the capacity to transport 1 MMTPA of diesel to Bangladesh. The supply will be done from Numaligarh Refinery Limited situated in Assam. This refinery supplies petroleum products to Bangladesh since 2015. (PIB, 2023)

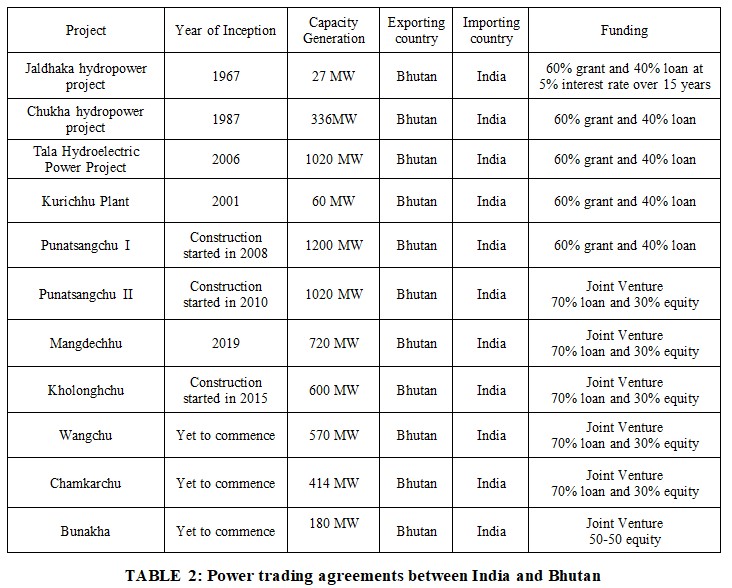

For hydro energy trading, numerous initiatives have been undertaken. The undergoing projects for cross border energy trading with Bhutan are listed in the table 2. There are also numerous undergoing hydroelectric projects among India, Nepal and Bangladesh as well.

Cooperation in the hydro energy sector has two aspects - Water management and Hydro Energy trading. The two aspects are complimentary in nature. The BBIN countries are prone to flood and drought. There is a chronic shortfall of energy in Bangladesh, while Bhutan and Nepal are yet to harness their energy potential. The BBIN countries share several transboundary rivers that are part of the Ganga-Brahmaputra-Meghna (GBM) basin. The GBM basin is home to around ten percent of the world’s population. Most of the people in the region are dependent on agriculture and other small-scale industries. However, water availability in this region is erratic and non-dependable. The quality of ground water available is also low. Climate change is another challenge faced by the people in this region. Therefore, there is a dire need for better water management.

The water and energy cooperation among the BBIN countries has two basic features: Firstly, cooperation is based on bilateralism, with each of the countries entering into separate energy development and trade agreement with India. Recently, electrical grid interconnections and hydro-energy cooperation has emerged with governments increasingly shifting from bilateral to multilateral energy-sharing agreements. Bangladesh is willing to connect its power grid with Nepal and Bhutan and expand the existing transmission capacity in both the eastern and north-eastern parts of India. Secondly, the countries of the sub-region follow a silo-ed approach in bilateral agreements, whereas water management and energy sharing are interlinked sectors.(Saklania, et. al., 2020). In water management and in energy trading agreements, the upper riparian state is in a dominant role. To ensure a win win situation, multilateral agreement is appropriate to give bargaining position to the smaller states than in bilateral agreements with India. India, on the other hand, can assure the smaller states who are suspicious of India’s hegemonic tendencies.

Under the umbrella of SAARC, many efforts were taken to enhance energy cooperation in South Asia. SAARC Energy Centre was created through the Dhaka Declaration in 2005 SAARC Summit held in Dhaka. South Asia Association for Regional Cooperation (SAARC) Regional Energy Trade study (SRETS) conducted under Asian Development Bank (ADB) regional technical assistance project brought out a report which was endorsed by SAARC. Although it identified that energy cooperation as the need of the hour for the developing region of South Asia, no concrete initiatives were taken at SAARC. At the sub-regional level in Eastern part of South Asia, there has been considerable developments which indicate prospects of multilateral cooperation among the countries of India, Bhutan, Nepal and Bangladesh.

Challenges for Energy Security

All the countries in the Eastern sub-region of South Asia, except Bhutan face energy deficit. Bhutan has a surplus amount of energy (hydropower) and hydropower energy is the export item which generates the highest foreign exchange reserves for Bhutan. But dominance of single fuel in the energy mix is a challenge for the energy sector in all countries of Eastern South Asia. Nepal and Bhutan, predominantly dependent on hydropower, face power capacity shortages due to water scarcity during winter. Harnessing the untapped potential of energy be it solar, wind or hydropower is a challenge for the sub-region because of inadequate infrastructure and lack of funds. Improving the energy supply and diversifying the energy mix of each country in the sub-region is of utmost importance.

Conclusion

The current policy of bilateralism works good for India but is looked upon with suspicion by the smaller riparian states. This is the reason for fallout of some of the initiatives for cooperation. The four countries can manage the challenges faced in the energy and water management by cooperating with each other. This will help them to reduce the cost of electricity, deal with scarcity in peak season, diversify their energy basket and also shift to cleaner energy sources. However, tapping all of the hydro power potential of the Himalayan region may lead to environmental hazards as the region is prone to earthquakes and landslides. An environment impact assessment should be made before starting any such projects.

References

Al-tabatabaie, K. F., Hossain, M. B., Islam, M. K., Awual, M. R., TowfiqulIslam, A. R. M., Hossain, M. A., Esraz-Ul-Zannat, M., & Islam, A. (2022). Taking strides towards decarbonization: The viewpoint of Bangladesh. Energy Strategy Reviews, 44. https://doi.org/10.1016/J.ESR.2022.100948

CEA. (n.d.). Executive Summary on Power Sector. https://cea.nic.in/wp-content/uploads/executive/2023/03/Executive_Summary_Feb_2023.pdf

Dhaka Tribune. (2022). PM Hasina: 100% electricity coverage a landmark success. https://www.dhakatribune.com/bangladesh/2022/03/22/pm-hasina-illuminating-every-house-is-a-great-achievement

Faijer, M. J., & Arends, E. (2017). Baseline Study Wind Energy Bangladesh. https://www.rvo.nl/sites/default/files/2017/05/baseline-study-wind-energy-bangladesh.pdf

Gyanwali, K., Komiyama, R., Fujii, Y., & Bajracharya, T. R. (2021). A review of energy sector in the BBIN sub-region. International Journal of Sustainable Energy, 40(6), 530–556. https://doi.org/10.1080/14786451.2020.1825436

International Energy Agency. (2022). WORLD ENERGY BALANCES 2022 EDITION - Database Documentation. https://www.iea.org/subscribe-to-data-services/world-energy-balances-and-statistics

Jha, R. (2010). Total Run-of-River type Hydropower Potential of Nepal. Hydro Nepal: Journal of Water, Energy and Environment, 7(7), 8–13. https://doi.org/10.3126/HN.V7I0.4226

Kuensel. (2022, December 22). PHPA-II Dam is ready. 2. http://phpa2.gov.bt/kuensel-paper-on-dam/ Mishra, P. (2019). OVERVIEW OF THE POWER SECTOR.

PIB. (2017). Three Years’ Achievements & Initiatives of the Ministries of Power, Coal, New & Renewable Energy and Mines. https://archive.pib.gov.in/archive2/erelease.aspx

PIB. (2019). Inauguration of Motihari-Amlekhganj (Nepal) pipeline by PM and PM Oli of Nepal. Press Information Bureau, India. https://pib.gov.in/newsite/PrintRelease.aspx?relid=193109

PIB. (2023). PM Narendra Modi and Bangladesh Prime Minister Sheikh Hasina jointly inaugurated the India-Bangladesh Friendship Pipeline. Press Information Bureau, India. https://pib.gov.in/PressReleaseIframePage.aspx?PRID=1908377

Power Sector at a glance. (2023). Ministry of Power, India. https://powermin.gov.in/en/content/power-sector-glance-all-india

Rahman, S. H., Wijayatunga, P. D. C., Gunatilake, H., & Fernando, P. N. (2012). Energy Trade in South Asia.

Saklania, Udisha. Shresthab, Padmendra P. Mukherjic, Aditi. Scott, C. A. (2020). Hydro-energy cooperation in South Asia: Prospects for transboundary energy and water security. Environmental Science and Policy, 22–34.

The Wire. (2018). Modi Announces 100% Electrification – But That Doesn’t Mean Everyone Has Power. https://thewire.in/government/narendra-modi-government-rural-electrification-power

UNCOMTRADE. (2022). 2021 International Trade Statistics Yearbook, Vol. I. https://comtradeplus.un.org/